A credit file in the United States is usually built through reported borrowing activity, not through income alone, savings alone, or payment history from the Philippines. For Filipinos who are new to the U.S., recently arrived on a work visa, studying, joining family, or rebuilding after a thin credit file, the safest path is to start small, use only products that report to the major credit bureaus, and keep every payment on time.

Why this matters →

Good U.S. credit can affect apartment applications, car financing, credit card approvals, loan pricing, and some utility or phone account deposits for Filipino households building a stable life in America.

What To Have Ready Before Applying:

- Legal name exactly as used on U.S. identity, immigration, school, or tax records.

- Current U.S. mailing address and phone number.

- Social Security number if eligible, or an ITIN where a lender accepts it.

- Proof of income or employment if the lender asks for it.

- U.S. checking account information for payments.

- A monthly budget that includes rent, food, transportation, remittances to the Philippines, and emergency savings.

Start With The U.S. Credit System

Credit in the U.S. depends on reported account behavior, not personal reputation or overseas banking history.

A strong banking record in the Philippines can help a person manage money, but it usually does not create a U.S. credit report by itself. U.S. credit reports are mainly built from accounts reported to Equifax, Experian, and TransUnion. The Consumer Financial Protection Bureau explains that secured cards, credit-builder loans, and certain starter credit products may help when the lender reports payments to the nationwide credit reporting companies.[a]

For a Filipino newcomer, the first goal is not to get a high credit limit. The first goal is to create a clean, reportable payment history. A low-limit card used carefully can be more useful than a large credit line that becomes hard to repay.

Tip: Before opening any credit product, ask one direct question: “Do you report this account to Equifax, Experian, and TransUnion?”

Know What Affects A Credit Score

The score is shaped by payment behavior, balances, credit age, new applications, and account mix.

FICO lists five broad categories used in FICO Scores: payment history, amounts owed, length of credit history, new credit, and credit mix. Payment history and amounts owed carry the largest general weight, although the exact effect can vary by credit profile.[b]

| Credit Area | What It Means | Practical Action |

|---|---|---|

| Payment History | Whether bills are paid on time. | Set automatic payments for at least the minimum due, then pay more manually when possible. |

| Amounts Owed | How much of the available credit is being used. | Keep card balances low and avoid using the full limit. |

| Credit Age | How long accounts have been open. | Keep the first good account open if there is no costly annual fee. |

| New Credit | Recent applications and new accounts. | Avoid applying for many cards or loans within a short period. |

| Credit Mix | Different account types, such as credit cards and installment loans. | Do not take unnecessary debt just to create a mix. |

Step 1: Open A U.S. Bank Account First

A bank account does not create credit by itself, but it supports safer credit management.

A checking account helps keep card payments organized, receive payroll, document income, and avoid missed due dates. Many Filipino workers and students also send remittances to family in the Philippines, so a clear budget should separate credit card spending from remittance money.

A debit card or prepaid card can be useful for spending control, but it normally does not build credit because the user is not borrowing and repaying money. A credit-building product must generally report repayment activity to credit bureaus.

Step 2: Use An SSN Or ITIN Correctly

Identity numbers help lenders match a person to the correct credit file.

Some noncitizens may be able to request a Social Security number if they work, attend school, or have a valid nonwork reason recognized by the Social Security Administration.[c]

An ITIN is issued by the IRS for federal tax purposes when a person needs a U.S. taxpayer identification number but is not eligible for an SSN. The IRS states that an ITIN does not authorize legal work in the United States, does not change immigration status, and does not serve as identification outside the federal tax system.[d]

IMPORTANT WARNING: A tax ID should never be used to misrepresent immigration, work, or identity status. Credit applications must be completed truthfully. If a lender does not accept an ITIN, look for another lawful option rather than forcing the application through incorrect information.

Step 3: Choose A Starter Credit Product

The first account should be simple, low-risk, and reported to the credit bureaus.

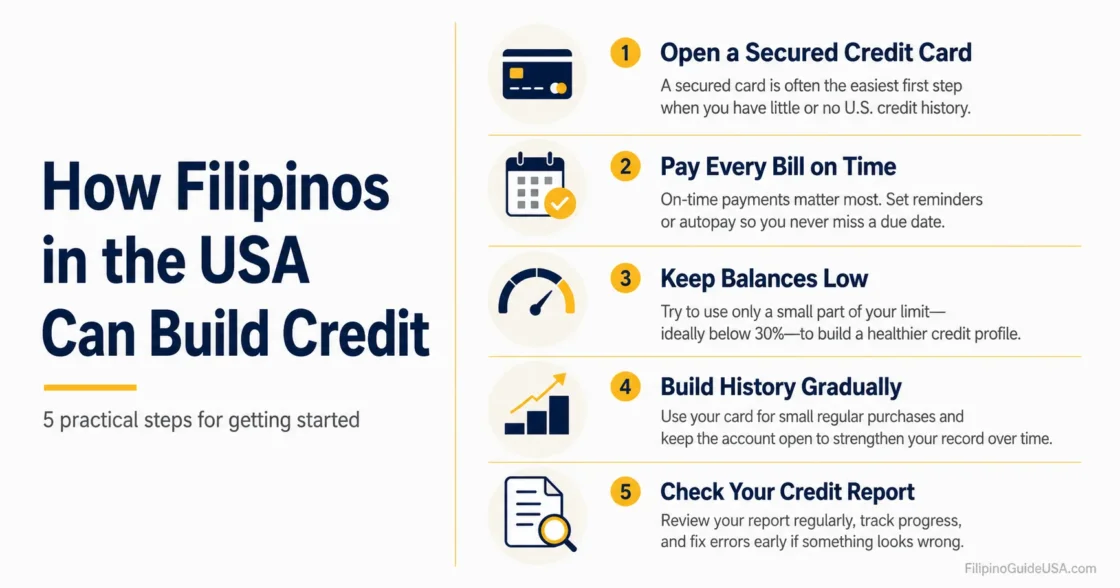

Secured Credit Card

A secured credit card is often the cleanest starting point. The cardholder pays a refundable security deposit, receives a small credit limit, uses the card for small purchases, and pays the bill on time. The deposit is not a monthly payment; it is security for the lender.

Credit-Builder Loan

A credit-builder loan is usually offered by some credit unions, community banks, or nonprofit financial programs. The borrowed amount is commonly held in a savings account while the borrower makes monthly payments. At the end, the borrower may receive the saved amount, depending on the product terms.

Authorized User Arrangement

A Filipino spouse, parent, adult child, or trusted relative may add a newcomer as an authorized user on an existing credit card. This can help only if the issuer reports authorized users and the main account has a clean payment history and low balance. The CFPB notes that an authorized user is generally not obligated to repay the debt, but issuers usually report authorized user status to credit bureaus.[e]

| Option | Best For | Main Risk |

|---|---|---|

| Secured Credit Card | Newcomers with no U.S. credit file. | Fees, high APR, or no bureau reporting if the card is poorly chosen. |

| Credit-Builder Loan | People who want a structured monthly payment. | Missed payments can hurt the file instead of helping it. |

| Authorized User | Trusted family situations with a strong primary cardholder. | The primary user’s late payments or high balance may appear on the authorized user’s report. |

| Retail Card | Limited use at one store when terms are clear. | High interest and temptation to buy more than planned. |

Step 4: Use The First Card In A Controlled Way

Small, predictable charges are enough to create useful credit history.

The safest routine is simple: place one or two small recurring expenses on the card, wait for the statement, and pay the full statement balance before the due date. Examples may include a phone bill, streaming subscription, or grocery purchase already planned in the monthly budget.

- Do not use the card as extra income.

- Do not carry a balance just to build credit.

- Do not miss the due date, even by a few days.

- Do not spend remittance money on credit card purchases unless the bill can still be paid in full.

- Do not close the first good account too early if it has no harmful fees.

Practical Example: A card with a $300 limit can still build credit. A person may use $30 to $60 during the month, then pay the full statement balance by the due date. The habit matters more than the size of the limit.

Step 5: Check Credit Reports Regularly

A new credit file should be monitored so mistakes do not remain unnoticed.

The three national credit reporting agencies permanently allow consumers to check reports from each agency once a week for free, according to the Federal Trade Commission.[f] Credit reports normally do not include every possible score, but they show account history, reported balances, payment status, addresses, names, and inquiries.

For Filipino readers, name consistency deserves extra attention. Credit report problems can happen when a person uses a maiden name on one record, a married name on another, a shortened nickname on a bank account, or a different order of given names and surnames. The legal name on credit applications should match the person’s official U.S. records as closely as possible.

Step 6: Dispute Errors With Documents

Wrong information should be challenged with the bureau and the company that supplied it.

If a report shows an account that does not belong to the person, a wrong late payment, an incorrect name, a wrong address, or an account status that does not match records, the dispute should include copies of supporting documents. The CFPB states that fixing an error generally means contacting both the credit reporting company and the company that provided the information.[g]

- Save the credit report confirmation number if available.

- Circle or identify the incorrect item.

- Explain what is wrong in clear language.

- Attach copies, not originals, of supporting records.

- Keep proof of submission, especially for mailed disputes.

- Check the report again after the investigation period.

Filipino-Specific Details That Often Get Missed

Several everyday situations in Filipino households can affect credit planning even when they do not appear directly on a credit report.

Philippine Credit History Usually Does Not Transfer Automatically

Loan payments, bank relationships, credit cards, and utility accounts from the Philippines usually do not appear on a U.S. credit report unless a specific lender or service has a process to use foreign data. A newcomer should plan as if the U.S. file starts from zero unless a lender confirms otherwise.

Remittances Affect Affordability

Sending money to family in the Philippines is common and meaningful, but it does not usually build U.S. credit. It still matters because lenders may review income and monthly obligations. A credit card payment plan should leave room for rent, food, transport, savings, and remittances without relying on the next paycheck too tightly.

Family Help Should Be Written Clearly

When relatives share housing, add someone as an authorized user, or help with a deposit, the arrangement should be discussed clearly. Who pays the bill, who can use the card, and what happens if the balance grows should be settled before the account is used.

Store Financing Should Be Treated Carefully

Furniture, phones, electronics, and appliance financing can look convenient for a newly arrived household. Before signing, the applicant should check the interest rate, late fees, promotion end date, and whether the account reports to credit bureaus.

Common Mistakes To Avoid

Many credit setbacks come from small habits repeated over time.

- Applying for several cards in the same month after one denial.

- Using the full credit limit because the card was approved.

- Paying only the minimum while the balance keeps growing.

- Ignoring the statement because automatic payment is set too low.

- Letting another person use a card without clear repayment rules.

- Believing that carrying interest is required to build credit.

- Using a prepaid card and expecting it to create a credit score.

- Missing a payment while traveling to the Philippines or changing addresses.

IMPORTANT WARNING: A missed payment can damage a young credit file more severely because there is little positive history to balance it. Before travel, relocation, or job transition, cardholders should confirm due dates, autopay settings, bank balances, and statement delivery methods.

When To Move From Starter Credit To Regular Credit

The next step should come only after several months of stable payment behavior.

After a starter card or credit-builder loan has been paid on time for several months, the account holder may ask whether the secured card can graduate to an unsecured card, whether the deposit can be returned, or whether the credit limit can be reviewed. This should be done without applying for several new products at once.

A practical timeline is behavior-based rather than calendar-based. The file should show on-time payments, low balances, correct personal information, and no unresolved reporting errors before applying for a car loan, apartment that requires credit screening, or higher-limit card.

Protect The Credit File From Fraud

Newcomers should protect identity records as carefully as payment history.

A credit freeze can limit access to a credit report and is free to place and lift, while a fraud alert tells businesses to verify identity before opening a new account. The FTC says a freeze does not affect a person’s credit score or ability to use existing credit cards, and fraud alerts can be placed by contacting one national credit bureau, which must notify the others.[h]

- Do not send SSN, ITIN, passport, or green card images through unsecured messages unless the recipient is verified.

- Be careful with “guaranteed approval” credit repair offers.

- Do not pay anyone to remove accurate negative information from a report.

- Use official credit report channels instead of lookalike websites.

- Review bank and card alerts after moving, changing phone numbers, or returning from travel.

Reliable Credit Habits For The First Year

A steady routine is more valuable than chasing fast score changes.

- Open a U.S. checking account and keep contact information current.

- Choose one starter credit product that reports to all three major bureaus.

- Use the account for small planned expenses only.

- Pay the full statement balance by the due date whenever possible.

- Keep balances far below the limit.

- Review credit reports for name, address, account, and payment errors.

- Wait before applying for more credit unless there is a real need.

- Protect identity documents and freeze credit if fraud risk appears.

Credit rules, lender requirements, bureau access, SSN and ITIN procedures, and financial product terms can change. Before applying, the applicant should verify the current terms directly with the bank, credit union, card issuer, IRS, SSA, and official credit-reporting resources.

Sources

- [a] Consumer Financial Protection Bureau, “What are some ways to start or rebuild a good credit history?” — supports the discussion of secured cards, credit-builder loans, and reportable payment history. The CFPB is a U.S. government consumer finance agency. ↩

- [b] myFICO, “What’s in my FICO Scores?” — supports the score category explanation. FICO is the company behind widely used FICO credit scoring models. ↩

- [c] Social Security Administration, “Request a Social Security number for the first time” — supports the SSN eligibility note for citizens and certain noncitizens. SSA is the official U.S. federal agency for Social Security numbers. ↩

- [d] Internal Revenue Service, “Individual taxpayer identification number” — supports the ITIN explanation and its limits. The IRS is the official U.S. federal tax authority. ↩

- [e] Consumer Financial Protection Bureau, “I was an authorized user on my deceased relative’s credit card account. Am I liable to repay the debt?” — supports the authorized user liability and reporting note. The CFPB is a U.S. government consumer finance agency. ↩

- [f] Federal Trade Commission, “You now have permanent access to free weekly credit reports” — supports the free weekly credit report access note. The FTC is a U.S. federal consumer protection agency. ↩

- [g] Consumer Financial Protection Bureau, “How do I dispute an error on my credit report?” — supports the dispute process with the credit reporting company and furnisher. The CFPB is a U.S. government consumer finance agency. ↩

- [h] Federal Trade Commission, “Is a credit freeze or fraud alert right for you?” — supports the fraud alert and credit freeze explanation. The FTC is a U.S. federal consumer protection agency. ↩