Opening a bank or credit union account in the United States depends on identity verification, address information, and the financial institution’s own account policy. Philippine citizenship by itself does not prevent a person from opening an account. Filipino immigrants, workers, students, permanent residents, U.S. citizens of Filipino heritage, and some temporary visitors may be able to apply when they can present acceptable documents and explain how the account will be used.

Why this matters →

A U.S. account can make payroll, rent, school payments, card use, and remittances to family in the Philippines easier to manage without relying heavily on cash.

Required Documents: Prepare originals when possible, because banks may not accept screenshots, photocopies, or expired identification.

Government-issued photo ID, such as a Philippine passport, U.S. driver’s license, state ID, green card, or Employment Authorization Document, depending on status and bank policy.

Social Security number, ITIN, or another bank-accepted identification number, such as passport number and country of issuance, alien identification card number, or another government-issued document showing nationality or residence.

Proof of U.S. address, such as a lease, utility bill, official mail, school housing letter, employer letter, or state ID with current address.

Date of birth and full legal name that match the documents used for the application.

Immigration, school, or work document if the bank asks for more context, such as I-94, visa page, I-20, DS-2019, I-797 approval notice, green card, or EAD.

Opening deposit, if the account type requires one.

U.S. phone number and email address for alerts, online banking, debit card activation, and fraud notices.

Important Notice: A Social Security number is not always required to get a bank or credit union account, but every financial institution must verify the applicant’s identity under federal customer identification rules. The Consumer Financial Protection Bureau states that a person does not need an SSN to get a bank or credit union account.[a]

Who Can Usually Apply?

This section separates eligibility from the documents a bank may ask to review.

Filipinos in the United States can generally apply for a deposit account if they can satisfy the bank’s identity, address, and risk-review process. The applicant may be a U.S. citizen, lawful permanent resident, temporary worker, international student, exchange visitor, spouse of a U.S.-based resident, or another lawfully present person. Some banks may also consider applications from visitors, but this is more likely to require an in-person branch visit and stronger proof of address or travel purpose.

Federal customer identification rules require banks to collect, at minimum, a customer’s name, date of birth, address, and identification number. For a non-U.S. person, the bank may collect an approved identification instead of a U.S. taxpayer identification number, depending on the institution’s procedures.[b]

Tip: A branch appointment is often better than an online application when the applicant does not yet have an SSN, has a short U.S. address history, or needs to use a Philippine passport as the main ID.

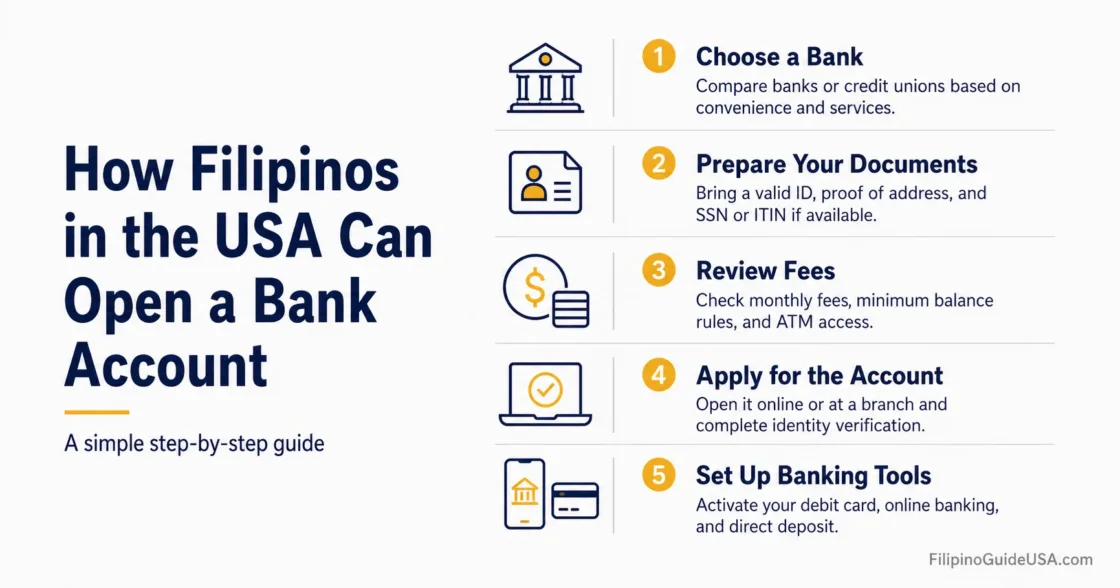

Step 1: Choose The Right Type of Account

The best account depends on whether the main need is daily spending, savings, payroll, or low-fee money management.

| Account Type | Best Use | What To Check Before Applying |

|---|---|---|

| Checking Account | Payroll, rent, groceries, debit card payments, bill pay, and everyday banking. | Monthly fee, minimum balance, debit card fee, ATM network, overdraft policy, and whether direct deposit can waive fees. |

| Savings Account | Emergency savings, short-term goals, and separating money from daily spending. | Minimum balance, withdrawal rules, interest rate, and transfer limits under the bank’s policy. |

| Low-Risk Checking or Safe Debit Account | First U.S. account, avoiding overdraft fees, and simple debit-card spending. | Whether the account blocks overdrafts, whether check writing is unavailable, and whether bill pay or online transfers are limited. |

| Credit Union Account | People who qualify for membership through location, employer, school, family connection, or community group. | Membership rules, branch access, mobile app quality, fees, and NCUA share insurance status. |

A low-risk account may be useful for a new arrival who wants basic banking without the risk of spending more than the available balance. The CFPB describes this type of account as one that does not allow overdrafts or check writing, making it suitable for first-time account holders or people who want to avoid overdraft fees.[h]

Step 2: Match Your ID To The Bank’s Rules

The application is easier when the applicant knows which document will serve as the identification number.

Many banks ask for two forms of identification, especially for non-U.S. citizens. The Office of the Comptroller of the Currency explains that for people other than U.S. citizens, an identification number may include a taxpayer identification number, passport number and country of issuance, alien identification card number, or another government-issued document showing nationality or residence and bearing a photo or similar safeguard.[c]

| Applicant Situation | Documents To Ask The Bank About | Practical Note |

|---|---|---|

| Filipino U.S. citizen or lawful permanent resident | SSN, U.S. driver’s license or state ID, green card if applicable, and proof of address. | This is usually the simplest path if the name and address match across documents. |

| New immigrant waiting for SSN | Philippine passport, immigrant visa or green card evidence, U.S. address proof, and any SSN application evidence if available. | Ask whether the bank can open the account with another accepted identifier or whether it requires the SSN first. |

| Temporary worker or exchange visitor | Passport, visa, I-94, work authorization document if applicable, approval notice, employer letter, and U.S. address proof. | Bring the document that explains the stay in the U.S., because the bank may ask why the account is needed. |

| International student from the Philippines | Passport, visa, I-94, I-20 or DS-2019, school ID if available, school address letter, and U.S. address proof. | A campus-area branch or credit union may be more familiar with student documents. |

| Applicant without SSN or ITIN | Philippine passport number and country of issuance, foreign government ID, alien identification number if available, and proof of U.S. address. | Policies vary. Calling the branch before visiting can prevent a wasted appointment. |

Important Notice: An ITIN is not a shortcut for opening a bank account. The IRS states that an ITIN is issued for federal tax purposes only, does not authorize work, does not affect immigration status, and is not issued solely for opening bank or investment accounts.[d]

Step 3: Prepare Proof of Address

Address proof is often where new arrivals have the most difficulty, especially when staying with relatives.

A U.S. address is usually required because the bank must know where the customer can receive official mail and account notices. A lease, utility bill, employer letter, school housing letter, government mail, insurance document, or state ID may help. If the applicant is staying with a relative, the branch should be asked in advance whether it accepts a signed household letter, the relative’s utility bill, and proof that the applicant receives mail at the same address.

Some banks may also ask for a foreign address or Philippine address history as part of their internal review. This does not mean the applicant cannot open an account; it means the bank is trying to complete its identity and customer profile records.

Tip: If the applicant recently arrived from the Philippines, it is useful to bring both the current U.S. address proof and one document showing the previous Philippine address, such as a passport record, Philippine ID, or official document if available.

Step 4: Apply In Person When The Documents Are Not Standard

An in-person application gives the branch a chance to review foreign documents that an online form may not recognize.

Online applications often work best for applicants who already have an SSN or ITIN, a U.S. address history, and a U.S. phone number. A Filipino applicant who is new to the country, using a Philippine passport, or waiting for an SSN may have a better chance of getting clear guidance from a branch representative.

Call the branch and ask which identification documents are accepted for a non-U.S. citizen or new U.S. resident.

Ask whether an SSN is required for the specific account or whether a passport number, ITIN, alien identification number, or other document can be used.

Ask what proof of U.S. address is acceptable, especially if staying with relatives or in temporary housing.

Ask whether the account requires an opening deposit and whether cash, debit card, check, or transfer can be used.

Ask whether the account includes debit card access, online banking, ACH transfers, check deposit, mobile deposit, and international transfer options.

Bring all documents to the appointment and make sure the name spelling is consistent across the passport, visa, address document, and application.

Procedure Note: A bank may approve the account during the visit, ask for more documents, or decline the application based on its own policy. A denial at one bank does not always mean another bank or credit union will make the same decision.

Step 5: Review Fees, Deposit Rules, and Overdraft Choices

The account should be usable for daily life without creating avoidable fees.

Before signing the account agreement, the applicant should review the monthly maintenance fee, minimum balance requirement, direct deposit waiver, ATM fees, paper statement fee, wire fee, international card fee, overdraft policy, and account closure fee. New arrivals should also ask when deposited checks become available and whether mobile check deposit is allowed immediately or only after the account has been open for a period set by the bank.

Overdraft settings need special attention. The CFPB states that institutions cannot charge overdraft fees on ATM transactions unless the customer has opted in, meaning the customer agreed to that coverage. The CFPB also notes that many banks and credit unions charge $30 or more per overdraft transaction.[i]

Important Notice: Do not opt in to overdraft coverage without understanding the fee. A debit card decline is usually less costly than a paid overdraft that creates a fee and a negative balance.

Step 6: Confirm Deposit Insurance Before Keeping Larger Balances

Deposit insurance protects eligible bank and credit union deposits when the institution is federally insured.

For banks, FDIC insurance applies at insured banks, and a person does not need to be a U.S. citizen or U.S. resident to have deposits insured. The standard maximum deposit insurance amount is $250,000 per depositor, per insured bank, for each account ownership category.[f]

For federally insured credit unions, the National Credit Union Administration states that the Share Insurance Fund insures individual accounts up to $250,000, and coverage is provided automatically when a person joins a federally insured credit union.[g]

Tip: Before depositing a large amount, verify the institution’s FDIC or NCUA insurance status directly through official lookup tools or by asking the branch for the insured institution name.

Step 7: Use The Account For Pay, Bills, and Remittances

A new U.S. account becomes more useful when it is connected to payroll, rent, utilities, and safe transfer habits.

After the account is open, the account holder can ask an employer about direct deposit, set up rent or utility payments, activate debit card alerts, and keep the account profile updated with the correct address and phone number. For Filipinos sending money to family in the Philippines, the account can also be used with a remittance provider, bank wire, ACH-linked transfer service, or debit-card transfer service.

Before sending money abroad, compare the transfer fee, exchange rate, delivery method, recipient name rules, pickup location, and cancellation process. The CFPB states that international money transfers can generally be cancelled within 30 minutes after sending, unless the recipient has already picked up the money or the funds have been deposited. It also explains that transfer problems can be reported up to 180 days from the date the funds are available, based on the receipt.[j]

Remittance Note: The recipient’s full name should match the Philippine bank account, cash pickup ID, or wallet profile. A small spelling mismatch can delay a transfer or require correction through the provider.

If You Are Denied An Account

A denial should be treated as a document and reporting issue to review, not as the end of the process.

If a bank or credit union denies the application, ask for the reason in writing. If the decision was based on a checking account report, ask which reporting company supplied the information. The CFPB advises consumers who are denied a checking account to request a copy of the checking account report, review it for errors, and dispute inaccurate information in writing.[k]

Ask whether the denial was caused by missing documents, address verification, identity verification, or past account history.

Ask whether a different account type is available, such as low-risk checking, safe debit, or a second-chance account.

Request the name of any checking account reporting company used in the decision.

Get the report, review the name, date of birth, address, and account history, and dispute any error.

Try another bank or credit union after correcting the issue or preparing stronger documents.

Notes For Common Filipino Situations

Different immigration and life situations can change which documents are easiest to use.

New Immigrants Waiting For A Social Security Number

Some new immigrants may receive or apply for an SSN through an immigration or work-authorization process. The Social Security Administration states that, in general, only noncitizens with permission to work from the Department of Homeland Security can get a Social Security number. If a person cannot get an SSN but needs to file taxes, the IRS provides ITINs for individuals who qualify for federal tax purposes.[e]

International Students From The Philippines

A student should bring the Philippine passport, visa page, I-94, I-20 or DS-2019, school ID if available, U.S. address proof, and school contact information. A branch near the school may be more familiar with student documents and campus housing letters.

Temporary Workers and Professionals

A temporary worker should bring the passport, visa, I-94, approval notice if available, EAD if applicable, employer letter, and proof of U.S. address. If direct deposit is needed for payroll, ask the employer whether a checking account, routing number, and account number are enough to begin payroll setup.

Spouses, Fiancé(e)s, and Family-Based Arrivals

A spouse or family-based arrival may be able to open an individual account if the bank accepts the documents. A joint account with a spouse or relative may be offered, but both account holders usually have access to the money and may be responsible for account activity. A joint account should not be opened unless both people understand the access, fee, and closure rules.

Frequent Travel Between The U.S. and The Philippines

Account holders who travel often should ask about foreign transaction fees, international ATM fees, debit card travel notices, account login from abroad, and the process for replacing a lost card while outside the United States. Keeping the U.S. mailing address, phone number, and email current can prevent card blocks and missed fraud alerts.

Before Submitting The Application

A short review at the branch can prevent delays after the account is opened.

Application Review: Confirm these items before signing or leaving the branch.

The legal name on the account matches the passport, SSN card, ITIN letter, green card, or other ID used.

The bank has the correct U.S. mailing address and contact number.

The applicant understands the monthly fee and how to avoid it, if a waiver is available.

The applicant understands overdraft settings and has not opted in by mistake.

The debit card delivery method and expected activation process are clear.

The account holder knows where to find the routing number and account number for payroll or transfers.

International transfer fees, ATM fees, and foreign card-use fees have been checked if the account will be used for travel or remittances.

Bank policies, tax rules, identity verification standards, and account fees can change. Before applying, the applicant should confirm the current requirements directly with the chosen bank or credit union and review official government sources for SSN, ITIN, deposit insurance, and consumer banking rights.

Sources

[a] Consumer Financial Protection Bureau — explains bank account options and states that a Social Security number is not required for a bank or credit union account. The CFPB is a U.S. government consumer finance regulator.

[b] Federal Deposit Insurance Corporation — explains customer identification program collection requirements for banks, including name, date of birth, address, and identification number. The FDIC is a U.S. federal banking agency.

[c] HelpWithMyBank.gov by the Office of the Comptroller of the Currency — lists identification numbers that may apply to people other than U.S. citizens. The OCC is a U.S. federal bank regulator.

[d] Internal Revenue Service — explains who may need an ITIN, how it is used, and why it is not issued solely for opening bank or investment accounts. The IRS is the U.S. federal tax authority.

[e] Social Security Administration — explains SSN eligibility for noncitizens and points people who cannot get an SSN toward IRS ITIN information when they need to file taxes. The SSA is the official U.S. agency for Social Security numbers.

[f] Federal Deposit Insurance Corporation — explains FDIC deposit insurance, including the $250,000 standard maximum deposit insurance amount and coverage for non-U.S. citizens or nonresidents. The FDIC is the official federal deposit insurer for insured banks.

[g] National Credit Union Administration — explains share insurance coverage for federally insured credit unions. The NCUA is the federal agency that regulates and insures federal credit unions.

[h] Consumer Financial Protection Bureau — explains low-risk bank accounts and how they can help first-time account holders avoid overdrafts. The CFPB is a U.S. government consumer finance regulator.

[i] Consumer Financial Protection Bureau — explains overdraft opt-in rules and common overdraft fee issues. The CFPB is a U.S. government consumer finance regulator.

[j] Consumer Financial Protection Bureau — explains consumer steps for international money transfer problems, cancellation timing, and error reporting. The CFPB is a U.S. government consumer finance regulator.

[k] Consumer Financial Protection Bureau — explains what to do after being denied a checking account and how to review a checking account report. The CFPB is a U.S. government consumer finance regulator.