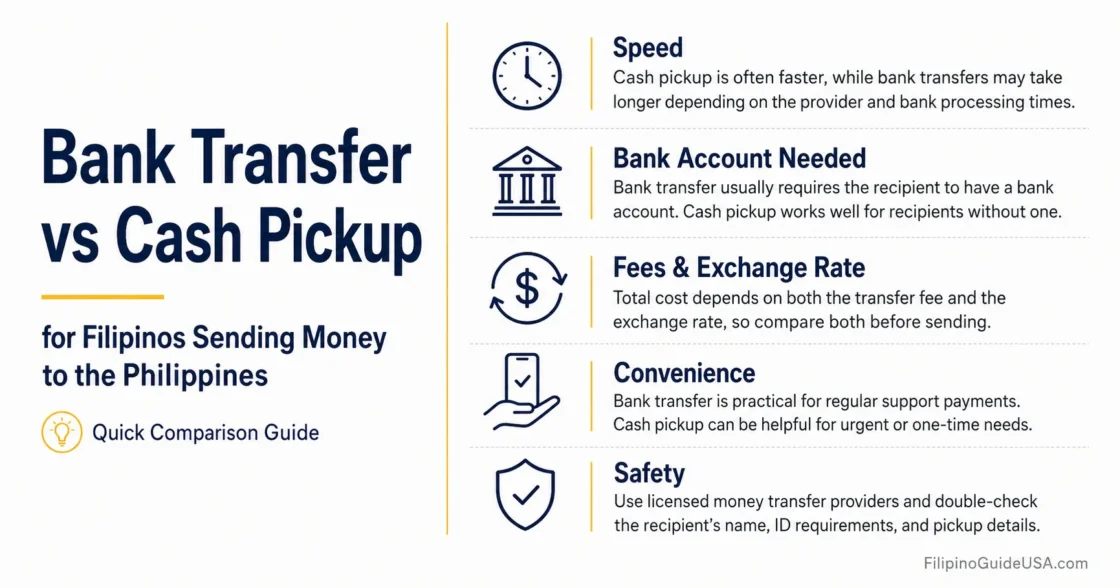

Choosing between a bank transfer and cash pickup is not only a question of speed. For Filipino families in the United States, the better option depends on how the recipient in the Philippines will use the money, whether they have a bank account, how urgent the need is, how easy it is to verify identity, and how clearly the sender can compare the exchange rate, transfer fee, delivery time, and final peso amount before paying.

Why this matters →

A remittance choice can affect how quickly family members in the Philippines receive support, how much money arrives after fees and exchange rates, and how easily a transfer can be traced if something goes wrong.

Prerequisites And Details To Confirm Before Sending:

- Sender’s full legal name, U.S. address, phone number, and valid identification if required by the provider.

- Recipient’s full legal name exactly as it appears on their valid ID or bank account.

- Recipient’s Philippine mobile number and city or province, especially for cash pickup.

- Bank name, account name, account number, and account type for bank transfers.

- Total amount to be paid in U.S. dollars, transfer fee, exchange rate, and expected amount in Philippine pesos.

- Expected delivery time and whether the transfer may be delayed by weekends, holidays, verification, or provider review.

- Receipt, transaction reference number, and provider contact details for tracking or error reporting.

Bank Transfer And Cash Pickup Serve Different Needs

This section explains the basic difference before comparing cost, speed, safety, and recipient convenience.

A bank transfer sends money directly to a bank account in the Philippines. Depending on the provider, the transfer may go to a traditional bank account, a mobile wallet linked to a financial institution, or another account-based receiving option. This method is usually easier to document because the money is tied to an account record.

Cash pickup sends money to a partner location where the recipient collects Philippine pesos in person. The recipient usually needs a valid ID and the transaction details provided by the sender. Cash pickup can be useful when the recipient does not have a bank account or needs physical cash quickly.

Both methods can be formal remittance channels when handled through regulated banks or money transfer companies. The Bangko Sentral ng Pilipinas explains that formal channels include banks and money transfer companies, while informal channels may not provide the same protection or recourse.[a]

Important Warning: Avoid informal arrangements such as sending money through acquaintances, travelers, or unverified social media contacts. They may seem convenient, but they can make the transfer harder to trace, harder to dispute, and harder to document for family budgeting or future financial records.

When Bank Transfer Is Usually The Better Choice

Bank transfer is often better when the recipient can receive money through an account and the sender wants a clearer transaction trail.

Bank transfer is usually the stronger option for regular family support, school payments, rent contributions, medical reimbursements, savings, and planned monthly remittances. It fits situations where the recipient has a bank account and does not need to stand in line at a pickup branch.

- Better for recurring support: Monthly family support is easier to track when deposits go to the same account.

- Better for recordkeeping: Bank deposits may leave a clearer account history for both sender and recipient.

- Better for larger planned transfers: Some senders prefer account-based transfers when the recipient does not need to carry cash after pickup.

- Better for recipients in busy areas: A bank transfer may avoid travel time, branch lines, and pickup location limits.

Tip: Before choosing bank transfer, confirm that the account name and account number are accurate. A small spelling mismatch or account detail error can delay the transfer or require extra provider review.

When Cash Pickup Is Usually The Better Choice

Cash pickup is often better when the recipient needs physical cash soon or does not have easy account access.

Cash pickup can be the practical choice for urgent family needs, relatives without bank accounts, recipients in areas where cash is still easier to use, or one-time support where an account transfer is not convenient. It may also help when the recipient’s bank branch is far away but a remittance partner location is nearby.

- Better for urgent cash needs: Pickup can be useful when the recipient needs money for transportation, groceries, medicine, or a same-day household expense.

- Better for unbanked recipients: It can work even when the recipient does not maintain a bank account.

- Better when account details are uncertain: If the recipient is unsure about bank information, a pickup transfer may prevent account-number mistakes.

- Better for short-term support: A one-time emergency transfer may be simpler as cash pickup if the provider’s pickup network is reliable in the recipient’s area.

Caution: Cash pickup depends on the recipient’s ability to present acceptable identification, visit the pickup location during operating hours, and keep the transaction number private. If the money is picked up, cancellation may no longer be available under U.S. remittance transfer rules.

Cost Comparison: Fee, Exchange Rate, And Final Peso Amount

The cheapest-looking option is not always the option that delivers the most pesos.

A remittance cost comparison should not stop at the transfer fee. The exchange rate can affect the final amount more than the visible service charge, especially when sending larger amounts. Some providers may advertise a low fee but use a less favorable exchange rate; others may charge a higher fee but deliver more pesos.

For U.S. international remittances, providers generally must show details such as transfer fees, taxes they collect, the exchange rate when applicable, the expected amount to be delivered, and when the money will be available. This makes it possible to compare the total transfer result before paying.[b]

| Decision Point | Bank Transfer | Cash Pickup |

|---|---|---|

| Best Use | Regular support, planned bills, savings, rent, tuition, or transfers where account records matter. | Urgent household needs, recipients without bank access, or situations where physical cash is needed. |

| Recipient Requirement | Correct account name, account number, bank name, and sometimes account type or branch details. | Valid ID, transaction reference, correct recipient name, and access to a pickup branch. |

| Speed | Can be fast, but may vary by provider, bank processing, verification, holidays, and cut-off times. | Often designed for fast availability, but pickup still depends on branch hours and provider review. |

| Record Trail | Usually easier to connect to account statements and household budgeting records. | Receipt and reference number are important; recipient should keep pickup confirmation if available. |

| Main Risk | Wrong account details, name mismatch, bank delays, or recipient bank charges. | ID mismatch, branch availability, lost reference number, or scams involving pressure to send cash. |

| Better For | Recipients who are banked, comfortable with account deposits, and do not need immediate cash in hand. | Recipients who are unbanked, need pesos quickly, or live near a trusted pickup location. |

The World Bank’s Remittance Prices Worldwide service can also help compare the cost of sending money by country corridor, including the sending country and receiving country selected by the user.[c]

Step 1: Start With The Recipient’s Real Situation

The best method is the one that the recipient can use safely and without friction.

Before comparing providers, the sender should confirm how the recipient actually handles money in the Philippines. A bank transfer may be logical for a recipient who pays bills online or uses an account for savings. Cash pickup may be more useful for a parent, sibling, or relative who relies on local cash payments and does not have reliable account access.

- Does the recipient have an active bank account under the same legal name?

- Can the recipient access the account without travel problems?

- Does the recipient need cash today, or can they wait for an account deposit?

- Is there a trusted pickup location near the recipient?

- Will the recipient be able to present valid ID with the correct name?

Practical Note: For elderly relatives, relatives in rural areas, or recipients with limited digital access, convenience may matter as much as price. A slightly cheaper transfer can become inconvenient if the recipient must travel far, miss work, or ask someone else for help collecting the money.

Step 2: Compare The Final Amount, Not Just The Fee

A fair comparison uses the amount the recipient is expected to receive in pesos.

The sender should compare at least three numbers before paying: the fee in U.S. dollars, the exchange rate, and the final amount expected in Philippine pesos. The final peso amount is the clearest comparison point because it reflects both the fee and the exchange-rate effect.

A simple comparison can be made by entering the same U.S. dollar amount in each provider’s quote screen and checking the expected peso delivery amount. If one option has a lower fee but delivers fewer pesos, it may not be the better value.

- Compare the same send amount across providers.

- Check whether the displayed exchange rate is locked or only estimated.

- Look for any message about recipient bank fees, foreign taxes, or third-party charges.

- Save or screenshot the quote before payment if the provider allows it.

- Keep the final receipt after payment.

Tip: If the transfer is urgent, compare both cost and availability time. A lower-cost option is less useful if it misses the date when the recipient needs the money.

Step 3: Check Delivery Time And Pickup Conditions

Speed claims should be checked against real-world limits such as branch hours, bank cut-offs, and identity review.

Bank transfers may be delayed by provider review, incorrect details, bank processing windows, Philippine holidays, U.S. holidays, or weekend timing. Cash pickup may appear available quickly, but the recipient still needs an open branch, acceptable ID, and matching transaction details.

For cash pickup, the sender should not assume every branch offers the same service hours or cash availability. The recipient should confirm the nearest pickup location before the sender pays, especially outside large cities.

Important Warning: A cash pickup transfer should never be sent to a person the sender has not personally verified. The Federal Trade Commission warns that wiring money can work like sending cash because, once sent and collected, it is usually difficult to recover.[d]

Step 4: Protect The Transaction Record

Good records help if the money is delayed, delivered incorrectly, or needs to be reported as an error.

The sender should keep the pre-payment disclosure, payment receipt, transaction reference number, expected delivery date, recipient details, and customer service contact information. The recipient should also keep pickup confirmation or account deposit confirmation when available.

Under U.S. remittance rules, a sender may have cancellation and error-resolution rights, including a limited cancellation window and a period for reporting certain mistakes. The details depend on the transfer and timing, so the receipt and provider instructions should be kept carefully.[e]

- Do not share the reference number in group chats or public posts.

- Send pickup details only through a trusted private channel.

- Confirm the recipient’s legal name before paying.

- Contact the provider quickly if the receipt has an error.

- Save all messages from the provider until the transfer is complete.

Which Option Fits Common Filipino Family Situations?

The right choice changes depending on whether the transfer is routine, urgent, account-based, or cash-based.

| Situation | Usually Better | Reason |

|---|---|---|

| Monthly Support For Parents | Bank transfer | It creates a repeatable account record and may be easier for budgeting. |

| Emergency Cash For A Relative | Cash pickup | It may be faster when the recipient needs pesos in hand and has a nearby pickup point. |

| Tuition Or School-Related Payment | Bank transfer | Account records may be easier to match with school payment planning. |

| Recipient Has No Bank Account | Cash pickup | The recipient can collect funds with valid ID if the provider’s requirements are met. |

| Large Planned Family Expense | Bank transfer | It may reduce the need for the recipient to carry a large amount of physical cash. |

| Recipient Lives Far From Pickup Centers | Bank transfer | An account deposit may avoid travel time and branch limitations. |

Use Only Regulated And Verifiable Providers

A provider should be chosen for traceability, clear disclosures, and formal customer support, not only advertising claims.

For transfers connected to the Philippines, senders should use banks, licensed money transfer businesses, or other formal providers that show clear fees, exchange rates, delivery timing, and customer support instructions. The BSP maintains guidance and regulatory materials for money service businesses, including remittance-related operators in the Philippines.[f]

A sender should be cautious when a person or page offers a special exchange rate through a private account, asks for payment outside a known provider, or pressures the sender to act immediately. A legitimate family remittance does not require secrecy, rushed payment, or bypassing normal provider disclosures.

Recordkeeping Note: For regular remittances, families may benefit from using one consistent receiving method. This makes it easier to review monthly support, compare transfer costs over time, and notice unusual delays or fee changes.

Common Mistakes To Avoid

Most remittance problems come from mismatched details, incomplete comparison, or rushing under pressure.

- Comparing only the advertised fee: The exchange rate can change the final peso amount.

- Using a nickname for the recipient: The name should match the recipient’s ID or bank account.

- Ignoring pickup location limits: Cash pickup depends on branch hours, ID rules, and local availability.

- Sending to someone under pressure: Urgent requests from strangers, online contacts, or impersonators should be treated as high risk.

- Deleting the receipt too soon: The receipt is needed for tracking, cancellation questions, or error reports.

- Assuming every transfer is instant: Provider review, bank cut-offs, holidays, or incorrect information can slow delivery.

Frequently Asked Questions

These answers address common decisions Filipino senders face when choosing between account deposit and cash pickup.

Is Bank Transfer Always Cheaper Than Cash Pickup?

No. Bank transfer may be cheaper in some cases, but the final cost depends on the provider’s fee, exchange rate, receiving method, amount sent, and any receiving-side charges. The better comparison is the final peso amount expected to arrive.

Is Cash Pickup Safe For Sending Money To Family?

Cash pickup can be safe when sent through a formal provider to a verified family member or trusted recipient. It becomes risky when the sender is pressured to send money quickly, asked to send to someone unknown, or told to keep the transaction secret.

What If The Recipient’s Name Is Spelled Differently?

The sender should correct the recipient name before paying. For bank transfer, the name should match the account record as closely as the provider requires. For cash pickup, the name should match the recipient’s acceptable ID. A mismatch can delay release of funds.

Which Method Is Better For Parents In The Philippines?

Bank transfer is usually better if parents have reliable account access and use the funds over time. Cash pickup may be better if they do not have a bank account, need immediate cash, or live closer to a pickup location than a bank branch.

Can A Sender Cancel A Remittance After Paying?

Cancellation depends on timing and transfer status. U.S. remittance rules generally provide a limited cancellation right, but cancellation may not be available once the money has already been picked up or deposited. The sender should check the provider receipt immediately after payment.

Before Sending, Recheck The Current Terms

Fees, exchange rates, delivery times, and pickup requirements can change without much notice.

Before paying, the sender should review the provider’s current quote, receipt terms, exchange rate, cancellation instructions, and error-reporting process. For bank transfers, the recipient’s account details should be checked one final time. For cash pickup, the recipient should confirm the pickup location, acceptable ID, and branch hours before the transaction is sent.

Remittance procedures, provider fees, exchange rates, and receiving rules may change over time. The safest approach is to verify the current details directly with the provider and, where relevant, consult official consumer protection or central bank resources before sending.

Sources

- [a] — Bangko Sentral ng Pilipinas, “OF Portal – FAQs on remittances.” Used for the distinction between formal remittance channels such as banks and money transfer companies and informal channels. The source is reliable because BSP is the central bank of the Philippines.

- [b] — Consumer Financial Protection Bureau, “Problems sending money to another country?” Used for the information remittance providers generally show before and after payment, including fees, exchange rate, expected delivery amount, and availability. The source is reliable because CFPB is a U.S. federal consumer finance agency.

- [c] — World Bank, “Remittance Prices Worldwide.” Used for comparing remittance costs by sending and receiving country corridors. The source is reliable because the World Bank is an international financial institution that maintains a global remittance price database.

- [d] — Federal Trade Commission, “What To Know Before You Wire Money.” Used for the warning that wire-style transfers can be difficult to recover after money is sent and collected. The source is reliable because the FTC is the U.S. federal consumer protection agency.

- [e] — Consumer Financial Protection Bureau, “What is a remittance transfer and what are my rights?” Used for sender rights related to remittance disclosures, cancellation, and error resolution. The source is reliable because CFPB publishes official U.S. consumer finance guidance.

- [f] — Bangko Sentral ng Pilipinas, “Registration of Pawnshops and Money Service Businesses.” Used for reference to money service business registration and remittance-related regulatory materials in the Philippines. The source is reliable because it is published by the Philippine central bank.