For many Filipino households in the United States, sending money to the Philippines is not a one-time transaction. It may support parents, children, tuition, medicine, home repairs, small business needs, or family emergencies. The cheapest method is not always the provider with the lowest advertised fee. The better measure is the final Philippine peso amount the recipient can actually use after the transfer fee, exchange rate, delivery method, and any receiving-side charge are included.

Why this matters →

A small difference in fees or USD/PHP exchange rate can reduce the monthly support a Filipino family receives back home.

Information To Prepare Before Sending:

- Sender’s full legal name, U.S. address, phone number, and email address.

- A valid government-issued ID if the provider requests identity verification.

- Recipient’s full legal name exactly as shown on the bank account, e-wallet, or pickup ID.

- Recipient’s Philippine bank account number, e-wallet number, or cash pickup details.

- The exact amount to send in U.S. dollars and the expected amount in Philippine pesos before payment.

- A copy or screenshot of the receipt, tracking number, delivery time, exchange rate, fee, and provider contact details.

The Cheapest Method Depends On The Recipient’s Situation

The lowest-cost option is usually the one that delivers the highest usable peso amount without adding access problems for the recipient.

For regular support, the most affordable starting point is usually an online transfer funded from a U.S. bank account and delivered to a Philippine bank account or verified mobile wallet. This type of transfer often avoids the higher costs that can come with card funding, walk-in cash service, or urgent cash pickup.

For a recipient without a bank account, cash pickup may still be the practical choice. It may cost more, but the transfer is not useful if the recipient cannot access the money. For a recipient who already uses a Philippine bank account or mobile wallet, direct deposit or wallet delivery may be cheaper and easier to track.

Overseas Filipino remittances are generally understood as private income transfers sent back by Filipinos abroad to support recipients in the Philippines.[a] For families that send money every month, comparing the total delivered peso amount can matter more than saving a single flat fee.

| Transfer Need | Usually Better Starting Point | Why It May Cost Less | Check Before Paying |

|---|---|---|---|

| Monthly family support | Online bank-funded transfer to a Philippine bank account | Lower payment cost and fewer cash handling steps | Final PHP amount, delivery day, and receiving bank details |

| Recipient uses GCash, Maya, or another wallet | Wallet delivery through a provider that supports the recipient’s wallet | Can be fast and convenient when limits are suitable | Wallet name match, wallet limits, and exchange rate |

| No bank account or wallet | Cash pickup | Not always cheapest, but may be the only accessible method | Pickup location, ID requirements, hours, and transfer code safety |

| Urgent support | Fast digital transfer or cash pickup | Saves time, but may carry higher fees or weaker exchange rates | Speed promise, cancellation rights, and recipient availability |

| Larger amount | Compare bank transfer, specialist remittance provider, and wire | A better exchange rate may outweigh a higher flat fee | Transfer limits, source-of-funds questions, receiving bank fees, and delivery date |

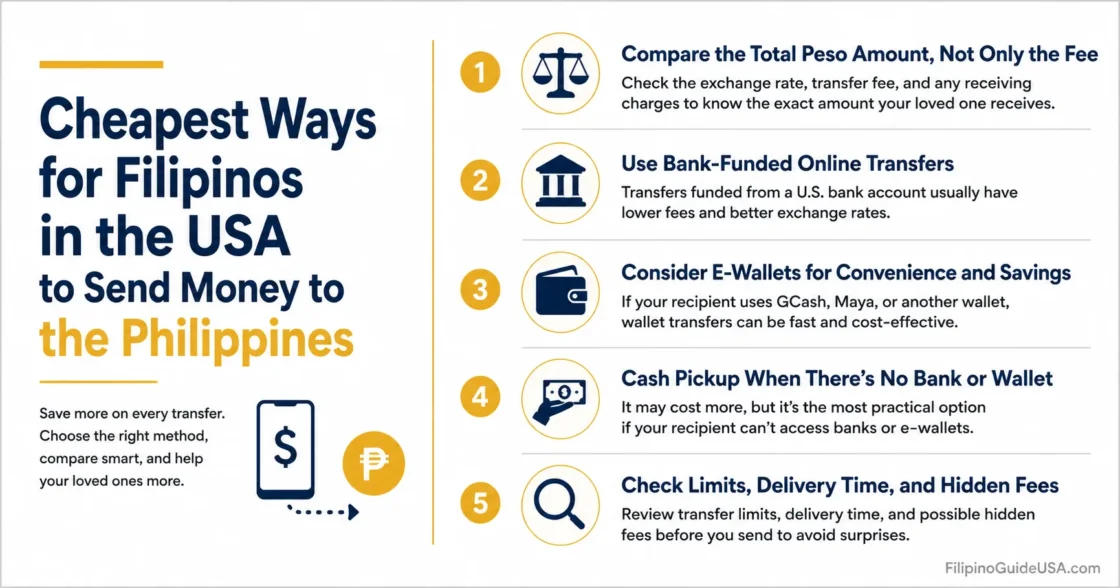

Step 1: Compare The Total Peso Amount, Not Only The Fee

A transfer advertised as “no fee” can still cost more if the exchange rate is weaker.

The true cost of a remittance has two main parts: the visible transfer fee and the less visible exchange rate margin. A provider may charge a low fee but offer fewer pesos per dollar. Another provider may charge a small fee but deliver more pesos because the exchange rate is better.

The practical test is simple: enter the same U.S. dollar amount with each provider, choose the same delivery method, and compare the final “recipient gets” amount in PHP before paying. Under U.S. remittance rules, providers generally must show information such as fees, exchange rate, total transfer cost, expected delivery amount, and availability date before or after payment, depending on the stage of the transaction.[b]

Tip: A $0 fee is not automatically the cheapest transfer. The exchange rate can quietly decide which option sends more pesos home.

Cost Check: Before paying, compare the same send amount across at least two providers. The sender should write down the fee, USD/PHP exchange rate, delivery time, and final PHP amount. The highest final PHP amount is often the better deal if speed and recipient access are equal.

Step 2: Choose The Right Delivery Method

The cheapest route can change depending on whether the recipient needs a bank deposit, wallet transfer, or cash pickup.

Bank Deposit

Bank deposit is often the best starting point for routine monthly support. It works well when the recipient has an active Philippine bank account and the sender does not need instant pickup. It can also reduce the risk of lost pickup codes or missed branch hours.

The sender should confirm the recipient’s legal name, bank name, account number, and any provider-specific field before paying. A minor spelling mismatch can delay delivery or require a correction process.

Mobile Wallet Delivery

Mobile wallet delivery can be convenient for recipients who already use a Philippine wallet for bills, transfers, or daily spending. It may be a low-cost option for smaller transfers, but wallet limits and verification status can affect how much the recipient can receive or hold.

The sender should check the wallet number, recipient name, and maximum receiving limit before sending. A wallet transfer that exceeds the recipient’s limit may fail, delay, or require support from the provider.

Cash Pickup

Cash pickup can be useful when the recipient lives far from a bank branch, does not have a bank account, or needs cash quickly. It may cost more than bank deposit or wallet delivery because the provider has to maintain a pickup network.

The sender should confirm the pickup branch, hours, accepted ID, exact recipient name, and tracking code instructions. The tracking number should only be shared with the intended recipient.

Step 3: Pick A Lower-Cost Payment Method

How the sender pays in the United States can affect the final cost.

Funding a transfer from a U.S. bank account is often cheaper than paying by debit card, credit card, or cash at a walk-in location. The tradeoff is speed. Bank-funded transfers may take longer, while card-funded or cash pickup transfers may be faster but more expensive.

Credit card funding should be treated carefully. In some cases, a card issuer may treat a money transfer as a cash advance or charge added card-related costs. If a card must be used, the sender should check both the remittance provider’s fee and the card issuer’s terms before paying.

DANGER: Do not send money to a person who pressures the sender to act immediately, claims a government agency requires wire payment, or says wire transfer is the only accepted payment method. The Federal Trade Commission warns that money sent by wire can be hard to recover once picked up by a scammer.[c]

Step 4: Use A Comparison Tool Before Large Or Repeated Transfers

A comparison tool helps the sender check whether a familiar provider is still competitive.

Provider pricing can change by amount, funding method, payout method, state, promotion, and exchange rate timing. For repeated transfers, a sender should compare costs again every few months instead of assuming the same app remains the cheapest.

The World Bank’s Remittance Prices Worldwide database provides country-corridor cost comparison data for smaller cross-border remittances, including transfers involving the Philippines.[d] It should be used as a comparison reference, not as the only decision point, because a sender still needs to verify the live quote before paying.

A practical comparison should use the same transfer amount, the same destination country, the same delivery method, and the same funding method. Comparing a bank-funded deposit from one provider against an instant cash pickup from another provider can lead to a misleading result.

Step 5: Read The Receipt Before And After Payment

The receipt is not just proof of payment; it is the sender’s record if something goes wrong.

Before paying, the sender should review the recipient name, amount, exchange rate, fee, total cost, expected peso amount, and delivery date. After paying, the sender should keep the receipt until the recipient confirms that the money arrived and is usable.

Federal consumer protections can apply to many remittance transfers over $15 made by a consumer in the United States to a person or company in another country, when the provider is covered by the rule.[e] These protections may include disclosures, proof of payment, cancellation options, and a way to dispute certain errors.

Receipt Habit: The sender should save the receipt, transfer number, provider support contact, exchange rate, and delivery date. If the recipient receives less than expected or cannot claim the money, these details help the provider investigate the issue.

Cheapest Ways By Common Filipino Household Need

The right option depends on the reason for sending, the recipient’s access, and how fast the money is needed.

For Monthly Support

For rent, groceries, utilities, school support, or family allowance, a bank-funded online transfer to a Philippine bank account is usually the first method to compare. Speed matters less when the transfer is planned, so the sender can choose a slower but cheaper route if the final peso amount is better.

For Emergency Family Needs

For urgent medical, travel, or household needs, the cheapest option may not be the best option if the recipient needs cash immediately. A fast wallet transfer or cash pickup may be worth the extra cost, but the sender should still check the final peso amount and verify the request through a trusted family contact.

For Parents In Provinces Or Smaller Towns

If the recipient lives far from a bank branch or relies on a local remittance partner, cash pickup or wallet delivery may be more practical. The sender should choose a provider with a nearby pickup partner or a wallet the recipient already uses. A cheaper bank deposit is not useful if the recipient must spend time and transportation money to access it.

For Tuition Or Larger Family Expenses

For larger transfers, the exchange rate becomes more important. A small difference in the USD/PHP rate can outweigh a flat transfer fee. The sender should compare at least two providers and confirm whether the receiving bank may deduct any charge before the recipient sees the full amount.

Common Cost Traps To Avoid

Many expensive transfers look cheap at first because only one part of the cost is visible.

- Only checking the fee: A low fee can hide a weaker exchange rate.

- Using credit card funding without checking the card issuer: Added card costs may make the transfer more expensive.

- Sending for cash pickup when bank deposit would work: Cash pickup can be useful, but it is not always the lowest-cost method.

- Ignoring the recipient’s access: A cheaper transfer can become costly if the recipient must travel far, wait in line, or cannot meet pickup ID rules.

- Relying on first-transfer promotions: A promotional rate may disappear after the first send, so repeat transfers should be compared separately.

- Not checking transfer limits: Wallet, bank, and provider limits can affect larger sends.

Tip: For monthly remittances, compare the provider again after the first promotional transfer. The regular rate may be different from the first-send offer.

What To Do If The Money Is Delayed Or The Amount Is Wrong

Fast action and complete records make it easier to resolve a transfer problem.

If a transfer is delayed, sent to the wrong name, received short, or not available by the promised date, the sender should contact the provider as soon as possible. The sender should have the receipt, transaction number, sender details, recipient details, screenshots, and a short explanation of the problem ready.

If the issue is not resolved, the sender may be able to use the provider’s dispute process or submit a complaint to the proper consumer protection agency. The sender should avoid posting personal transfer numbers, ID images, account numbers, or private family details on social media.

IMPORTANT WARNING: If the recipient cannot pick up the money because the name does not match the ID, the sender should not create a second transfer until the first one is corrected, cancelled, refunded, or clearly resolved by the provider.

Frequently Asked Questions

These answers address the practical questions Filipino senders often face before choosing a remittance method.

What Is Usually The Cheapest Way To Send Money From The USA To The Philippines?

For planned transfers, a bank-funded online transfer to a Philippine bank account or verified mobile wallet is usually the first option to compare. The sender should judge the option by the final PHP amount, not only the advertised transfer fee.

Is Cash Pickup More Expensive Than Bank Deposit?

It can be. Cash pickup often costs more because it depends on physical payout locations and agent networks. It may still be the right choice when the recipient does not have a bank account, needs cash urgently, or lives near a reliable pickup branch.

Are “No Fee” Transfers Really Free?

Not always. A provider can charge no visible transfer fee but use an exchange rate that gives fewer pesos per dollar. The sender should compare the final PHP amount against another provider before paying.

Should A Sender Use A Credit Card To Send Money?

A credit card should be used carefully. Card-funded transfers may cost more, and the card issuer may add charges depending on how the transaction is treated. A bank account or debit method may be cheaper, but the sender should confirm the live quote and card terms.

Can A Sender Cancel An International Money Transfer?

Many international transfers can be cancelled within a limited time after payment if the money has not already been picked up or deposited. The sender should check the provider’s cancellation instructions on the receipt and act immediately.

What Should The Recipient Check Before Money Is Sent?

The recipient should confirm the correct spelling of the legal name, bank or wallet details, pickup ID, wallet limit, and nearest pickup branch if cash pickup is used. Small detail errors can delay delivery.

Before Paying For The Transfer

A final review protects both the sender in the United States and the recipient in the Philippines.

- Compare the same amount across at least two providers.

- Look at the final PHP amount, not only the U.S. dollar fee.

- Check whether the exchange rate is promotional or regular.

- Choose a delivery method the recipient can actually use.

- Confirm the recipient’s name, bank, wallet, or pickup details before payment.

- Save the receipt until the money is received and usable.

- Recheck provider terms, limits, fees, and USD/PHP rates before each transfer.

Transfer costs, limits, identity checks, cancellation details, delivery times, and USD/PHP exchange rates can change. Before paying, the sender should review the provider’s current pre-payment disclosure and the recipient should confirm access to the selected bank, wallet, or pickup location.

Sources

- Bangko Sentral ng Pilipinas — OF Portal: FAQs on remittances — Used for the Philippine context on overseas Filipino remittances and why these transfers matter to families and the economy. (Official central bank of the Philippines.) ↩

- Consumer Financial Protection Bureau — Problems sending money to another country? — Used for remittance disclosure, cancellation, delivery, error, refund, and complaint-rights information. (U.S. federal consumer financial protection agency.) ↩

- Federal Trade Commission — What To Know Before You Wire Money — Used for wire-transfer scam warnings and safe-payment cautions. (U.S. federal consumer protection agency.) ↩

- World Bank — Remittance Prices Worldwide — Used for the role of corridor-based remittance cost comparison when checking provider prices. (International financial institution and global remittance price data source.) ↩

- MyCreditUnion.gov — Sending Money Overseas — Used for U.S. remittance transfer examples and the general scope of consumer protections for many overseas transfers. (Official National Credit Union Administration consumer resource.) ↩